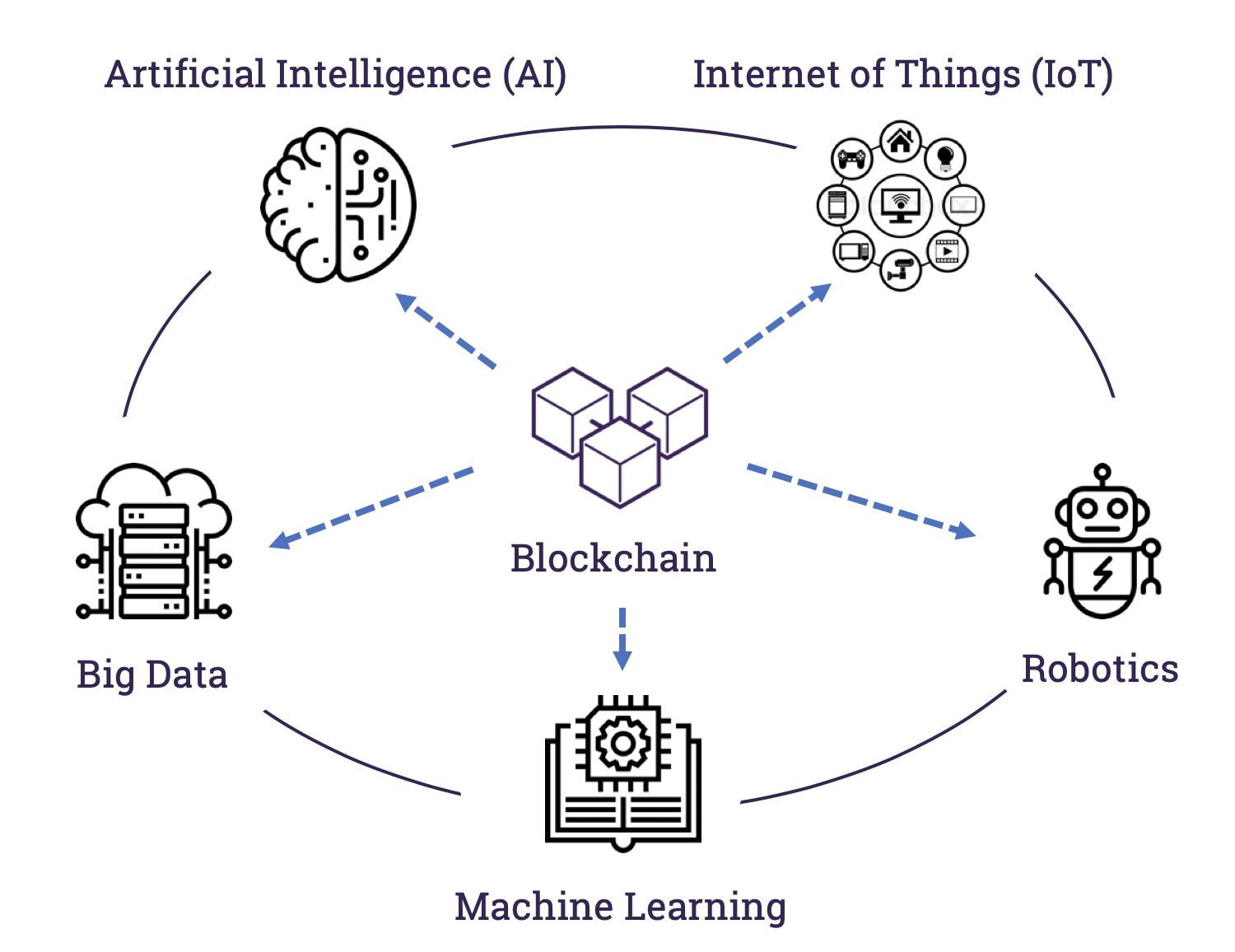

In this exciting podcast, our 50th, we had the great pleasure of having Magda Ramada Sarasola, EMEA Insurtech Innovation Leader, at Willis Towers Watson return to Insureblocks. In this fireside chat we discussed the emergence of a new stack – the convergence of blockchain, AI, IoT, big data, machine learning and robotics.

This podcast sits at the epicentre of a pivot we’re doing at Insureblocks for 2019. In addition to reporting stories on blockchain within the insurance industry, Insureblocks is going to embrace three new themes:

- Cover new industries: finance, supply chain logistics, food and agriculture, automobile and transportation, and healthcare. The aim is to investigate their blockchain learnings and facilitate the sharing of best practice across industries

- Investigate how blockchain sits with this new technology stack that includes AI, IoT, machine learning, big data, and robotics. We believe that while they’re noteworthy the potential these technologies have individually is limited but once combined as a stack there is the “multiplier” effect to their potential

- Deep dive into the legal and regulatory blockchain environment and of course best practices for establishing effective governance within blockchain networks

What is Blockchain?

In the initial days blockchain was often referred to as a shared excel database. Of course, now we know that blockchain is a lot more than that. Today blockchain can be looked as this ledger that participants who don’t know each other and don’t necessarily trust each other can transact without the need for an overseeing central actor. Transactions of value can be:

- Exchanged without being corrupted or changed

- Validating their authenticity and confirm that whoever is sending the value actually owns it

Consequently for Magda, blockchain is a sociological innovation. It enables peer-to-peer markets to work without centralised authorities. This has impact not just onto the peer-to-peer world but also onto the enterprise and business world whose ecosystems are highly dysfunctional. It gives enterprises peer-to-peer enablement which makes blockchain so interesting.

It’s a new governance paradigm that changes the way we organise markets and transactions of value in the broadest sense of the word (i.e. digital and physical assets).

Data the lifeblood of insurance

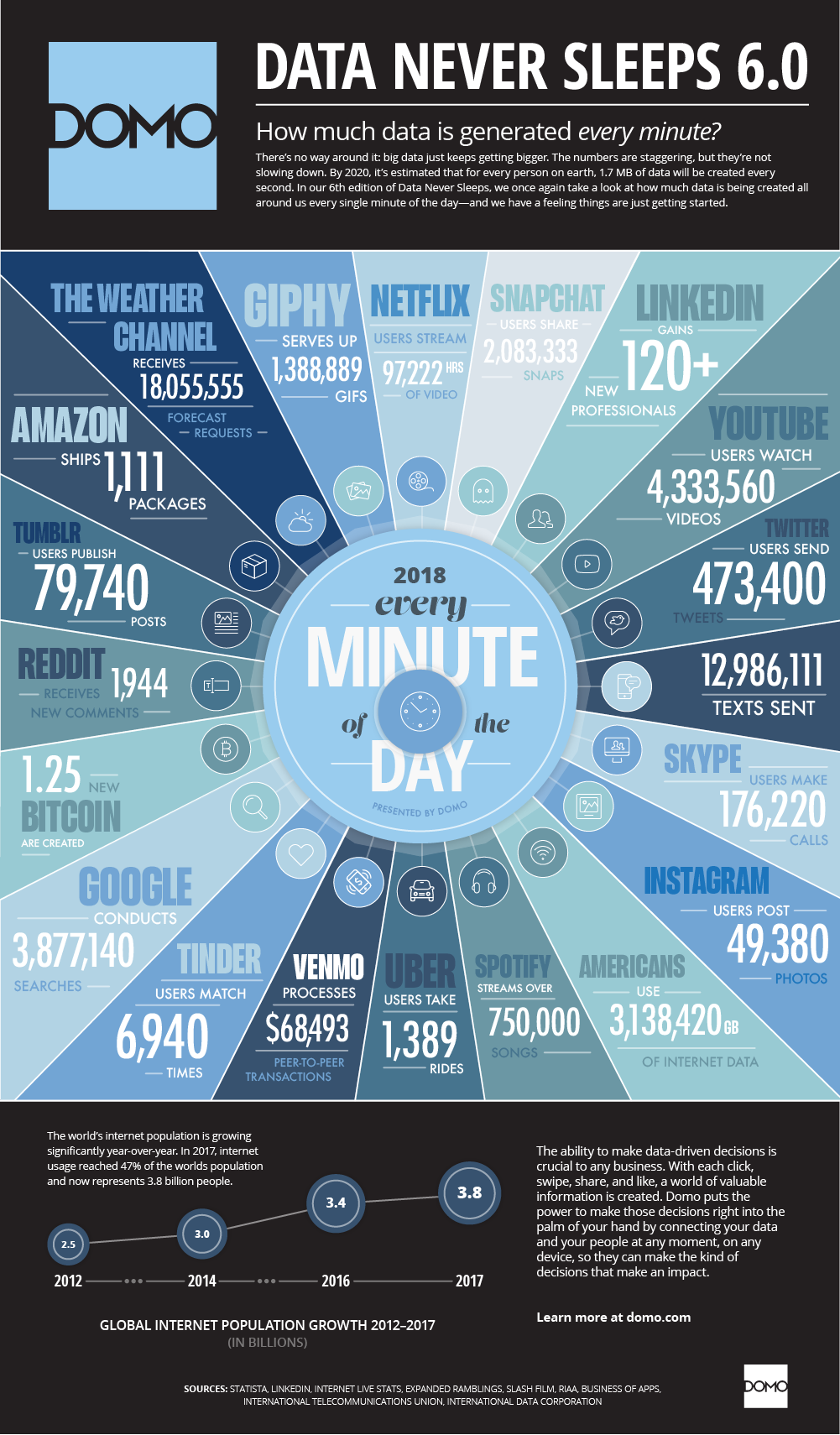

August last year, Insureblocks interviewed Bill Pieroni, CEO of ACORD– (Ep. 21 ACORD: data standards for blockchain in insurance) where he stated “Data is the lifeblood of the insurance industry, which fundamentally works by examining data to quantify risk”. Over the last few years the nature, type and amount of data that is becoming available to the insurance industry has radically changed. Sandip Patel, Global Managing Director for insurance from IBM, stated that on Insureblocks that “Data is the new natural resource” and he mentioned three important points:

- Volume of data is changing – 2.5 quintillion (a thousand raised to the power of six {1018}) bytes of data is produced on a daily basis (as reported by Forbes in May 2018)

- Type of data from both structured and unstructured

- Temporal factor of data

Source: Domo – Data Never Sleeps 6.0

Magda recognises the “mind-blowing” amount of data that is being produced on a regular basis that it is very difficult to define what the actuarial value of that data is. Insurance industry was quite late to embracing big data. One of the reasons was that they didn’t have enough transactional data at a high frequency like ecommerce does for example. That has changed, over the last few years, as the insurance industry recognises that there is a lot of data that it doesn’t own that is being generated by other players that has been proven to actually add value in assessing the riskiness of an individual or of a certain asset / situation.

However due to the large amount of data that is produced it is important to have a clear data strategy that understands:

- Type of data you have / don’t have

- Type of data you need and where to get it

- Knowing how to structure that data

- How to make best use of that data

- What that data adds in value as opposed to what you already have

- The necessary infrastructure to deal with the data and secure the data

The Netflix paradigm

For Magda, the insurance industry may be facing what she calls the “Netflix paradigm”.

What’s driving all of the insurance industry’s pillars of innovation is data and how we use that data. The problem is that most of the data is not owned by the insurance industry. Partnerships are made to access data from Fitbit, Under Armour, Apple Watch, and many others. It’s really difficult to price that data today, because data is not distributed and it’s sitting in centralized repositories that are owned by different actors.

Not so long ago, Netflix was able to stream a lot of movies that it didn’t own. However, when the market increasingly used streaming and binge watching on Netflix, that became the prevailing business model that cannibalised the channels that traditional content owners had. This forced the traditional content owners to raise their price for their content in order to eat into Netflix’s margins. However, Netflix had anticipated that move and had already started producing its own content and has now become one of the main content generators globally. Why? Because they were sitting on lots of data about behaviour about what people watched and when and they were able to use that to generate very targeted content.

Today the insurance industry is able to access data it doesn’t own from third parties like Fitbit. However, at some point the value of the data will be clear and insurance players may not be able to access that data anymore.

The new stack

Next year there is an estimated 20-25 billion IoT devices coming online. All these devices will produce raw data which we aren’t able to process into intelligence. Not only that but they’re being communicated on the internet which is insecure and open to cyber criminal activity.

Some innovative insurance companies have been looking at emerging technologies like AI, IoT, machine learning, big data, robotics, drones, telematics and a whole range of other technologies. However these have been looked at individually instead as a new stack and thus the ROI is limited.

Data vaults

At the present moment we are producing a large amount of data which is only going to increase on a yearly basis. Numerous questions arise on how we can keep the data secure, communicate it in a secure way, keep it free from tampering or nefarious actions, and ensure that it can be monetized and used by its rightful owner.

Today, whilst you own your data and are in charge of it in some extent, it is being copied and used by companies. There is a need for identity solutions and data self-sovereignty. Unfortunately does solutions are not mature enough today and a new infrastructure is required to enable them. This coupled with the fact that it will take a long time for people to realise the value of their data and how their data is being used.

Blockchain can help in bringing a solution by providing its users with the ability to be custodians of their own data. The way this would work is that people will have a data vault which can contain their digital identity, their FitBit data, their driving behaviour and medical data for example.

For example, today to get a drink in a bar in the US you have to prove you are over 21 years old and have to show your driver’s license. However, that driver’s license contains your address which you may not wish to share with the bartender. With a secure data vault, that contains your driver’s license, it can essentially automatically validate that you are over 21 without sharing your address. If people have those vaults and objects have their vaults, data becomes an inherent part of every actor in an economy and its individual historical data that cannot be corrupted.

A car is an example of an object data vault who streams data. The car can validate its data such as how it is being driven and maintained. The day the car is sold it can be sold with its data vault.

Alongside user vaults and object vaults we can also have vaults of behavioural data and many other vaults in the future. For Magda, that is the future where data is being distributed as opposed to centralised and it is secured in a cryptographic manner.

Need for a new infrastructure – blockchain coalition, cross industry and government initiatives

We need to focus on the things that blockchain enables that we cannot do with other technologies. Magda illustrates two key points:

- Data stored within a data vault cannot be corrupted even by the owners of the data. So for the first time users can be true custodians of their own data

- Blockchain frontier – i.e. how the data gets into the vault, that it comes from trustworthy sources such as a bank or a government institution. This will require a new infrastructure that can connect all these validators to an immutable and distributed ledger.

For example if you go into a bank that bank will have systems where they can look at your credit worthiness, they look at your behaviour, they look at Equifax and then they will validate the data. If they put that into your vault whenever you go to another bank, they don’t have to repeat it, as the KYC would already have been done from a trusted source. As it is stored into your data vault they will also know that the data hasn’t been tampered with.

For this to happen it will require blockchain coalitions and cross industry and government initiatives to build the necessary infrastructure.

Oracles and IoT the weakest link?

When looking at innovation in general and specifically at the new stack we realise that it isn’t just about blockchain. Blockchain is dependent upon getting reliable validated data into it. These comes from oracles which can take the form of IoT devices. Securing real-time data streams from IoT is not easy. As you cannot corrupt the smart contracts on the blockchain there is a clear case for trying to corrupt the oracles. There is a need to secure the oracles.

Maximising ROI by moving from individual technologies to the new Stack

There is a clear business case for merging these emerging technologies into a new stack. These technologies are doing very different things and if you really want to have a quantum leap in terms of how you develop a new business model or enable a new way of doing things, you need the combination, you need the new stack.

IoT are a great source of instant access to data. Machine learning and computer vision can extract data from numerous sources such as what is your sentiment from micro facial expressions to the distress in your voice. Machine learnings and certain algorithms are critical for data ingestion and for the analytics of that data.

Big data implies that we are sitting on a very large amount of data ready for us to use. The reality though isn’t quite that. The data isn’t ready. It needs to be structured, it needs to be cleaned from what is noise and what is valuable. For that you need advanced analytic tools, machine learning, AI, computer vision augmented related to be able to incorporate things like a human behaviour with the data and the physical reality around them.

All these technologies really work well in combination. Blockchain enables a way of having distributed markets and distributed value and interactions with people without them being centralised. For that to happen you need to know who the people are, how they behave and you need to understand them. This requires a smart contract to be truly smart. It can only achieve this by having a layer of machine learning that has access to data for it to learn from.

Thus, to maximise ROI we need to ensure that we look at the business case and then determine what set of technologies is appropriate for that business case. It may be a small set of technologies, it may be the entire stack or it may be legacy technology. The key is to always start from the business case and not to look for a problem that this technology can answer.

Future of risk and its pricing

Having the technologies from the new stack and hyper granular data sitting on those data vaults we have what Magda calls fourth generation solutions that can react in time to events and to behaviour. This means in the future we should be able to have products that adapt in their structure as in clauses what they cover, what they don’t and price themselves in an almost real-time fashion.

Another future possibility is one where for certain types of risks and products we may not need an underwriter to actually underwrite. For example, future car insurance will be on a smart contract that can read exactly how the car is being driven, used, and maintained. The smart contract will also understand the driver’s driving patterns and automatically price the risk.

You can neutralise the risk through a coded mutual for certain type of risks, where you have smart contracts dealing with pricing the risk, assessing the risk, pricing risk, pulling it, generating a vehicle like an insurance security and placing it in a distributed capital market. Part of the risk for that car insurance can be accepted by individuals around the world such as one in China or in Australia that have a certain risk appetite that has been assessed by their respective smart contracts. In such a future you are bridging the risk to capital journey in a decentralised and automated way.

Parametric insurance

Parametric insurance is the low hanging fruit as it is straightforward to process if you have the right data input you can automate it very quickly. The question is does parametric insurance require a blockchain? In most cases probably not, but there are some where it does. In those cases where it makes sense from a consumer perspective to buy a product where they want to make sure the insurer could not stop the policy from being executed.

Your Turn

Thank you, Magda, for this fireside chat and for sharing your views on the new stack. If you’d like to meet Magda, make sure to attend the upcoming Blockchain for Insurance Conference here in London on the 18thto 19thof June 2019.

Spread the love